Differentiated regional development for the EPLF

20 Ocak 2016 - 12:59 'de eklendi ve 5310 kez görüntülendi.

20 Ocak 2016 - 12:59 'de eklendi ve 5310 kez görüntülendi.

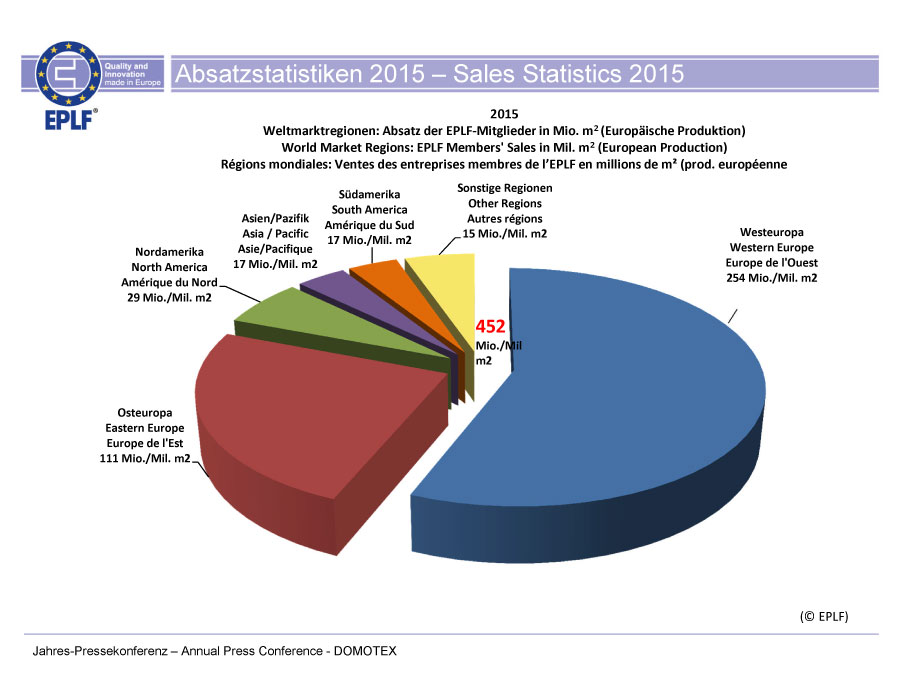

In 2015, worldwide sales of 452 million m² of European-produced laminate flooring (467 million in 2014) were reported by the 20 Ordinary Members of the EPLF (i.e. the manufacturers of laminate flooring). The resulting minus of 3.1 % is relativized in view of a Turkish member having left the EPLF at the end of 2014. Once again, growth rates varied between regions during 2015 ‒ Western Europe (including Turkey) was somewhat weaker, whereas Eastern Europe saw a slight upturn. Figures rose positively as well in Asia, and the biggest gains were recorded in North America. EPLF laminate flooring sales in South America for 2015 also showed an upward trend.

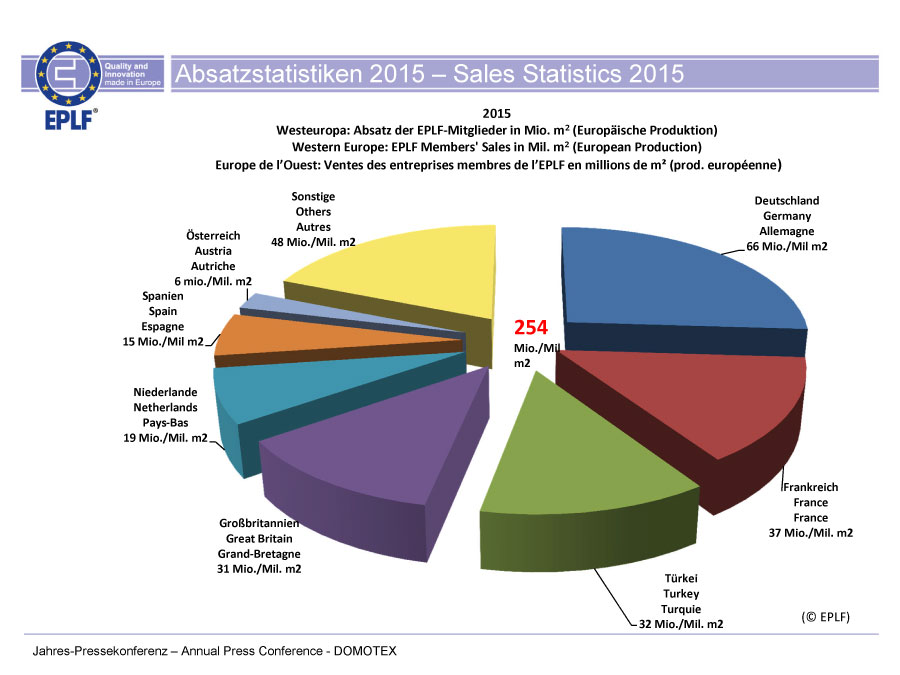

With one Turkish member having left the EPLF, the Western European sales of the laminate flooring industry (including Turkey) fell from 282 million m² in 2014 down to 254 million m² in real figures in 2015, i.e. a plunge by 10 %. In Germany – the largest single regional istanbul escort market in Central Europe – the substitution trend continued: The EPLF believes that a shift in favour of what is known “LVT flooring” is the reason for the decline on the German market down to around 66 million m² (prev. year 69 million m²), showing a minus of 4.6 %. However, from the EPLF’s point of view, the German flooring market will continue to dominate in the future by a wide margin – not only as a sales market but more than ever as the country of origin with an estimated more than 230 million m2 production volume.

Also included in the EPLF sales statistics for Western Europe is Turkey, where laminate sales for the Association experienced another significant drop during 2015, showing a decline of approx. 44 % down to 32 million m² (prev. year 57 million m²). The reasons behind this are complex: a major Turkish member having left the EPLF at the end of 2014, and the anti-dumping proceedings brought forward by the Turkish Ministry of Economy against some German flooring manufacturers, which ran until summer 2015, have both contributed to the decline. Another factor to be considered, according to the EPLF, is the general weakening of the Turkish economy. Despite worsening figures, Turkey remains the third-largest target market for EPLF members.

France has shown a slight downturn with 37 million m² (prev. year 39 million m²) and in 2015 now occupies second place in Europe. The United Kingdom, despite a booming construction market, did not continue its positive upward trend for the EPLF members, showing slight losses of 3 % with a sales figure for 2015 of 31 million m² (prev. year 32 million m²), which puts the country in a strong fourth place right after Turkey. The Netherlands market grew in 2015 with + 8 %, and at 19 million m² (prev. year 18 million m²), still managed to retain fifth place. With sales of 15.3 million m² (prev. year 14.6 million m²) and roughly + 5 %, Spain holds on to sixth place.

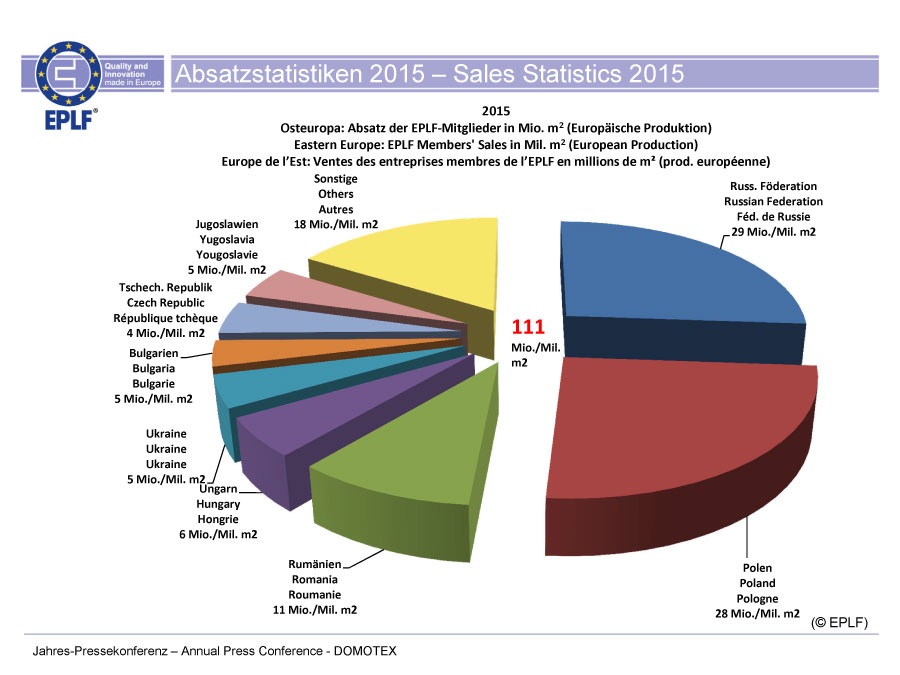

Despite a difficult situation in Eastern Europe during 2015, EPLF laminate sales were able to keep up in this region. Indeed, at 111 million m² (prev. year 110 million m²), European laminate flooring producers achieved a slight increase in that region of 1 %. In Russia, 29 million m² were sold (prev. year 28 million m²), which resulted in a growth rate of

2 %. Meanwhile the association learned that, due to different reasons, about 20 million m2 out of the EPLF members’ Russian production are not included in the statistics. At any rate, the 2015 outcome once again puts Russia ahead of Poland in the sales ranking – Poland beylikduzu escort saw an improvement of 7 % (prev. year 6%) up to 28 million m² (prev. year 26 million m²). The subsequent places in the ranking are occupied by Rumania with 11 million m² (prev. year 11 million m²), Hungary with 6 million m² (prev. year 6 million m²), Bulgaria with 5 million m² (prev. year 4 million m²) and the Ukraine with a good result after all of nearly 5 million m² (prev. year 8 million m²).

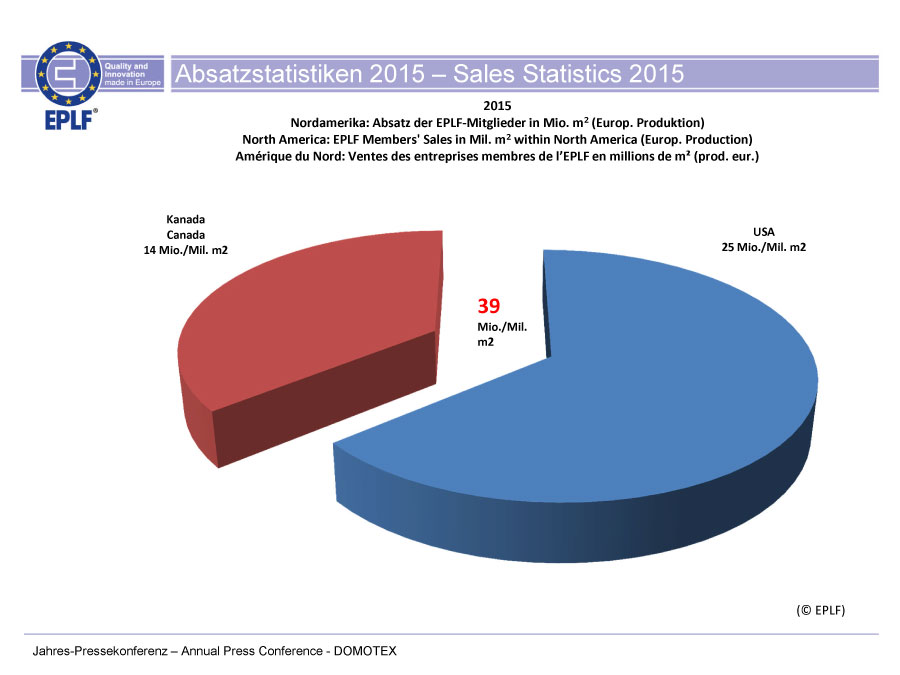

The EPLF sales curve for North America has been rising steeply since 2013 and that trend has continued in 2015, with +32 % up to 39 million m² (prev. year 29 million m²). At 25 million m² (prev. year 18 million m²), the USA saw gains in 2015 of 37 %, Canada achieved a good increase of 24 % in 2015 with 14 million m² (prev. year 11 million m²).

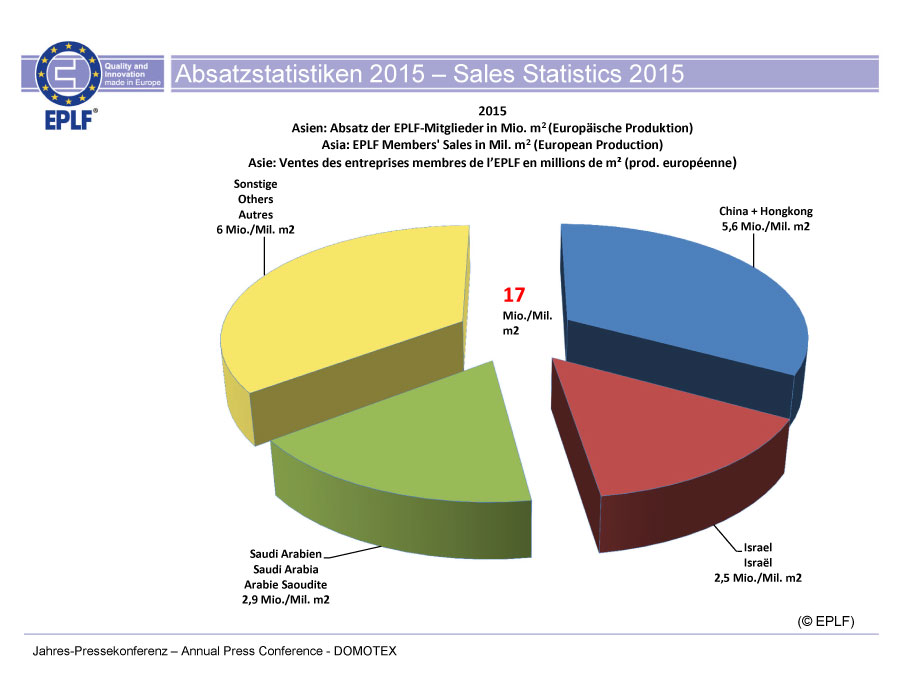

Total sales in 2015 of European-produced laminate in Asia Pacific stand at around 17 million m² (prev. year 15 million m²), which means an increase of 14 % (following +20 % the prev. year). Again, the biggest growth was registered in the Chinese market, which includes Hong Kong. Exports from high-end products made in Europe are increasingly well received here – 2015 saw sales of 5.6 million m² (prev. year 5 million m²), which equates to an increase of 10 % over the previous year. Israel has improved slightly at 2.5 million m² (prev. year 2.2 million m²) and Saudi Arabia has registered good growth with 3 million m² (prev. year 2 million m²). The markets in India and Australia, with their traditionally low turnover level, have also shown comparatively pleasing growth in 2015.

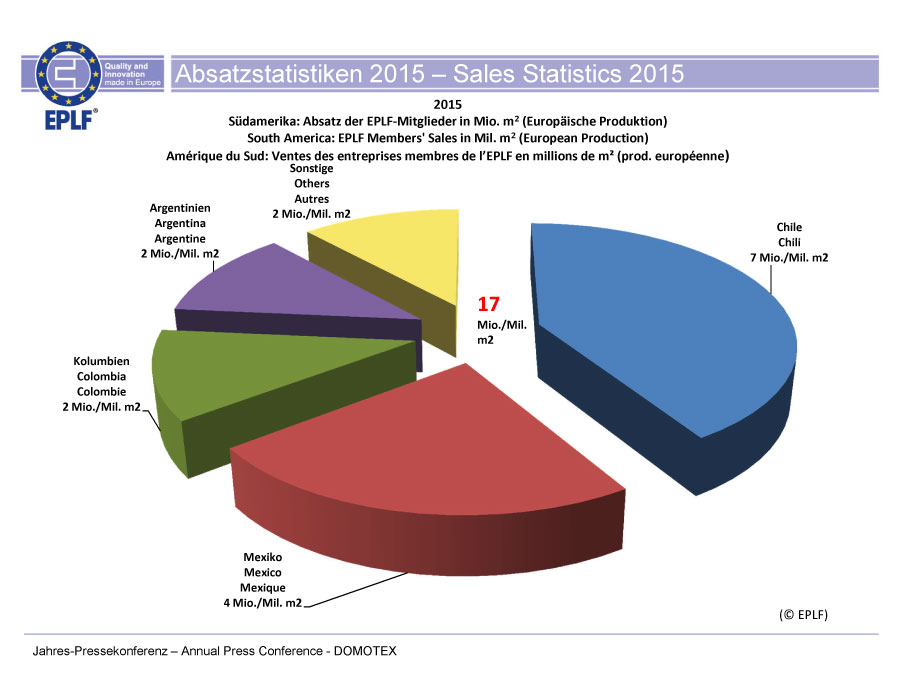

South America showed an overall positive trend in 2015 with 17 million m² (prev. year 16 million m²) and + 9 %. Sales in Mexico reached around 4.5 million m² (prev. year 3.9 million m²), also Argentina showed better results with 1.8 million m² (prev. year 1.4 million m²). Compared with the previous year, the Chilean market remained stable with sales of 7 million m² (prev. year 7 million m²).

Dünya Bir Kez Daha İstanbul Prohunt’da Buluşacak!

Dünya Bir Kez Daha İstanbul Prohunt’da Buluşacak! Pandemide yıldızı parlayan karavanların dünyasını Karavanist’te keşfedin

Pandemide yıldızı parlayan karavanların dünyasını Karavanist’te keşfedin İstanbul Prohunt

İstanbul Prohunt IAAF Istanbul Art & Antique Fair

IAAF Istanbul Art & Antique Fair Markaworld Instagram’da izlenmeye değer

Markaworld Instagram’da izlenmeye değer